How Being Nonbinary Affects Getting Life Insurance: Why Underwriters Look At Gender

Applying for life insurance presents unique challenges for those who identify as nonbinary (or simply "NB"). Because many insurance providers haven't updated their underwriting guidelines, applicants are still asked to identify as either male or female.

But, why does a life insurance company ask you to list a gender when you don't identify with one or the other? What are your options for disclosure if you're NB or trans people? Keep reading this guide to find out the answers to these questions and more! We'll also talk about how being nonbinary effects getting life insurance and what you can do to get the best coverage possible.

Why Do Life Insurers Ask About Your Gender?

It is standard industry practice to ask for applicants to disclose this because there is a link between gender and mortality. While the rates vary from country to country, women generally have longer lifespans than men.

Since a shorter life means a whole life insurance or term life insurance policy is more likely to be paid out, women usually pay lower premiums than men for all types of life insurance, even if they get policies with the same death benefit. Montana is currently the only place in the United States where the underwriting process is unisex – gender does not play a role in applications.

But is there any significant difference between the life expectancy of cisgender people and that of NB people? For now, there's no definitive answer, largely because the NB community has only recently become visible and accepted. This means there isn't enough data for actuaries to charge a higher or lower premium for cisgender, NB, or transgender life insurance.

As awareness builds, companies in the United States may consider changing their underwriting process to allow people to tick off "non-binary" in their application and offer more accurate life insurance rates for NB individuals.

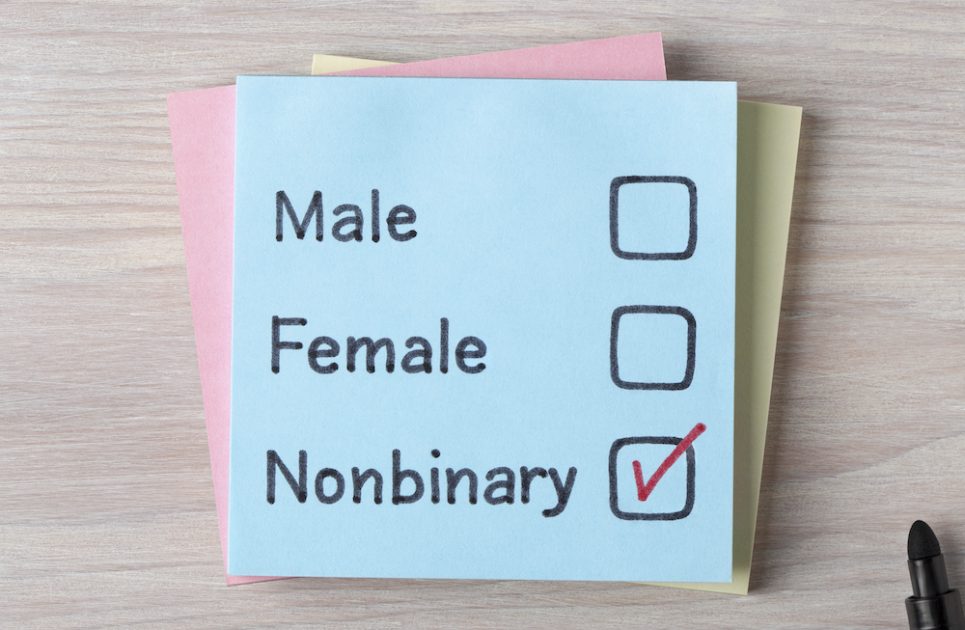

Why Can't I Tick A Box On My Application That Says I'm NB?

Many insurers still only list two options for term or permanent life insurance: male or female. You currently can’t list that you are NB on your life insurance applications, even if you identify as such.

This is not meant to be a discriminatory process, although that’s an unintended consequence – companies ask this question for the sole purpose of calculating your premiums.

Will Being Nonbinary Disqualify Me From Obtaining Life Insurance?

No. The law protects the rights of NB and transgender people seeking life insurance, and companies are not allowed to prevent you from obtaining life insurance based on gender.

Choosing Gender Identity For Your Insurance Application

Until life insurers update their definitions of gender, there is no uniform set of guidelines for what companies expect on your insurance application. Here are the three options that may be presented to genderfluid, nonbinary, or transgender applicants:

Assigned At Birth

Your chosen whole or term life insurance provider may ask you to tick off your gender at birth in your application, regardless of your chosen identity.

What You Identify As

In some cases, life insurance companies will compute your policy based on the gender you identify as. If NB applicants want to side-step this binary problem, they can look for insurance providers who issue policies based on unisex rates, aka blended male/female rates.

After Affirming Surgery Or Treatment

Companies may base an applicant's choice on any gender-affirming treatment they have had, such as breast reduction or hormone therapy. The date of your last surgical procedure or how long you’ve been taking drugs for hormone therapy can affect this choice.

Why Do Insurance Providers Ask For Your Surgical Or Hormone Treatment History?

Anyone trying to obtain life insurance policies will be asked to disclose their surgical history as it will affect health risks – and, consequently, premiums. Apart from any surgeries for medical conditions, nonbinary or transgender individuals may undergo affirmation (formerly known as gender reassignment) surgery to eliminate gender dysphoria. For example, a person who is assigned male at birth but identifies as nonbinary may choose to undergo breast augmentation to more closely align with their identity.

Many of these surgeries are cosmetic and do appear to not increase mortality rates in nonbinary people. However, a significant percentage of those who undergo breast augmentation do end up needing a second surgery within a year, which increases health risks. This could potentially affect underwriting rates.

Likewise, hormone therapy may affect cardiovascular health or the likelihood of developing certain health conditions. While there’s still no scientific consensus on their correlation, United States insurers still require applicants to disclose any regular medication they are taking – including hormonal drugs – to assess if this will affect an applicant's life span.

How Gender Affects Your Life Insurance Application

Apart from affecting your mortality rates, this factor is linked to the likelihood of developing certain health issues or dying from various events. Here's a list of factors which the life insurance industry has tied to gender and how they can affect your premium.

Body Mass Index (BMI)

Although it’s a flawed standard, many insurers consider an applicant's build or BMI to gauge the likelihood of premature death or later health problems. The rate tables differ for men and women, as there are different standards of "healthy" weights for one's height depending on gender. If you fall outside of that healthy range, your risk for developing health problems increases, and as such, you may be charged higher premiums.

Alcohol Consumption

Men are considered more likely than women to binge drink and thus suffer alcohol-related illnesses like cirrhosis or liver damage. These illnesses result in a shorter life expectancy, which can drastically increase your premiums.

Risk-Seeking Behavior

Apart from being more likely to engage in physically demanding jobs, men are also more likely than women to perform riskier tasks or actively seek out riskier activities. These activities could result in fatal accidents for the insured. So, all things being equal, a man would have higher life insurance premiums.

Smoking

While the gap between the number of male and female smokers has narrowed, there are still more men than women who smoke. Smoking is tied to cardiovascular disease and increased chances of suffering a fatal heart attack.

Many companies will consider you a non-smoker for insurance purposes if you've been smoke-free for at least five years, but even non-habitual smoking can have a negative impact on your health and, consequently, your premiums. This is why companies charge male smokers higher rates compared to female smokers and non-smokers.

FAQs About Applying For Insurance When You're Nonbinary

Is there a way for me to get life insurance coverage without identifying as male or female?

Yes. Your first option is to find an insurer who will base your policy on unisex rates. You may be required to undergo a medical examination for underwriting purposes.

If your employer offers group life insurance, many companies allow you to be covered under a unisex policy. This will provide you with coverage without undergoing a potentially embarrassing or invasive medical exam. This will also allow you to get the benefit of low group insurance rates but with the downside of a smaller death benefit and more limited coverage. Keep in mind that you may also lose this policy if you switch jobs because the policy is with your employer, not you.

If you want increased coverage without undergoing a medical examination, you can ask your employer how to upgrade your group policy through their provider. You can also consider policies that are guaranteed issue, such as final expense insurance.

Can my insurance provider disclose my gender or sexuality?

As a general rule, life and health insurance companies cannot disclose these to third parties without your express permission. Most should have a privacy policy that protects their personal information.

There are very few exceptions to this rule on non-disclosure:

- For providing treatment to an insured patient or facilitating payment for said treatment

- Assisting law enforcement in an investigation

- For any purpose, so long as the company does not identify the insured individuals

Keep in mind that this is not an exhaustive list of exceptions. Regardless of the situation, an insurance provider is usually required by the law to give as little personal information about insured individuals as possible.

Ask A Financial Advisor How To Get The Best Policy

Identifying as nonbinary impacts how you apply for life insurance and the premium you will be charged. If you're looking for an insurer that can give you the best coverage, get in touch with a finance expert. Contact us as Wesley Insurance, LLC to find out how you can provide for you and your loved ones without compromising your privacy rights!